http://doi.org.10.15198/seeci.2018.45.103-120

RESEARCH

IMAGE OF WHITE BRANDS IN THE FOOD SECTOR ACCORDING TO THE PERSPECTIVE OF THE SPANISH CONSUMER

IMAGEN DE LAS MARCAS BLANCAS EN EL SECTOR ALIMENTARIO SEGÚN LA PERSPECTIVA DEL CONSUMIDOR ESPAÑOL

IMAGEM DAS MARCAS BRANCAS NO SETOR ALIMENTICIO SEGUNDO A PERSPECTIVA DO CONSUMIDOR ESPANHOL

Mónica Matellanes Lazo1

Has a bachelor’s degree in Advertising and Public Relations from the Complutense University of Madrid. Master of Commercial Management and Marketing Management from Esic-Madrid and PhD from the University of Valladolid.

She has worked in Communication and Marketing within the wine area and is currently Associate Professor of these subjects at Miguel de Cervantes European University in Valladolid. She has had several stays as an Erasmus professor and a Curator at foreign universities in Portugal (Lisbon, and Ponte de Lima) and in the United Kingdom (Aberystwyth). Author of several research articles in the area of communication, latest appearances in Sphera, Comm Research, Egitania, Vivat Academia, Reason and Word. She is co-author of the book Quality and differentiation in the wine sector (published by the University of Évora).

Alba Villota Mancebo2

Graduated in ADE and in Advertising and Public Relations from Miguel de Cervantes European University in Valladolid and she has an MBA from the Universidad Pontificia de Comillas. She has done several consultancy works and has been part of the communication team of the Provincial Office of Palencia. Her Final Degree Project on the distribution of white brands was graded Outstanding. Currently, she works in the Marketing Department of the distribution company Seur.

Raquel Fernández Merino3

Holds a degree in Advertising and Public Relations from Miguel de Cervantes European University in Valladolid and in Sociology from Uned. With a Master’s degree in business and political communication and a Master’s degree in protocol and event management, both from Camilo José Cela University. Her Final Project was about the consumption of wine in the DO Ribera del Duero and it was graded Cum Laude Outstanding. She is currently responsible for communication in social networks of the communication office of Valladolid Deputation.

1European University Miguel de Cervantes de Valladolid. Spain.

2European University Miguel de Cervantes de Valladolid. Spain.

3Diputación de Valladolid. Spain.

ABSTRACT

The value of private labels in the food sector has varied greatly in recent years. The marketing mix is facilitating distributors that white markings can compete at the same level as the manufacturer. Currently, many consumers believe that white brands offer quality products at a very competitive price, important aspect, strategically seen. This allows the market to supply a consumer’s profiles which is excluded of the target willing to pay for the brand, offering him what he wants: more product in exchange of of the same ammount of money. An amount that, due to the commercial packaging, ends up being the same or greater profits for the companies, and increasing business activity. It also allow the big brands to create their own “white brands” in order to monetize their excedents. Which, by any other means, might end up being mere un-productive items in the companie’s balance? This research aims to analyze the perception of these brands with a local show in Spain and know the valuation of consumers; You like to know which distributor enjoys greater notoriety through their white markings.

KEYWORDS: Brand, Distribution, Marketing, Perception, Consumer, Public.

RESUMEN

El valor de las marcas blancas en el sector alimentario ha variado mucho en los últimos años. El mix del marketing está facilitando a las distribuidoras que las marcas blancas puedan competir al mismo nivel que las del fabricante. En la actualidad, muchos consumidores opinan que las marcas blancas ofrecen productos de calidad a un precio muy competitivo, aspecto importante visto estratégicamente. Ello permite al mercado suministrar a un perfil de cliente que queda excluido del público objetivo dispuesto a pagar el plus de marca, ofreciéndole lo que quiere: más producto por el mismo dinero que, debido a la compartimentalización comercial, termina resultando en ingresos iguales o superiores y en cifras de negocio ascendentes. También permite a las marcas, a través de sus propias “marcas blancas” dar salida a sus excedentes a cambio de líquido sin dejar de atender a sus clientes. Unos excedentes que, de otra forma, quedarían reducidos a ítems improductivos dentro del balance de las empresas. Esta investigación pretende analizar la percepción de estas marcas con una muestra local en España y conocer la valoración de los consumidores; al igual que saber qué distribuidora goza de mayor notoriedad a través de sus marcas blancas.

PALABRAS CLAVE: Marca, Distribución, Marketing, Percepción, Consumidor, Público.

RESUME

O valor das marcas brancas no setor alimentício há variado muito nos últimos anos. O mix do marketing está facilitando as distribuidoras que as marcas brancas podem competir ao mesmo nível que as marcas do fabricante. Na atualidade, muitos consumidores opinam que as marcas brancas oferecem produtos de qualidade por um preço bastante competitivo, aspecto importante visto estrategicamente. Esta investigação pretende analisar a percepção destas marcas com uma amostra local na Espanha e conhecer a avaliação dos consumidores; ao igual que saber qual distribuidora tem maior notoriedade através de suas marcas brancas.

PALAVRAS CHAVE: Marca, Distribuição, Marketing, Percepção, Consumidor, Público

Received: 14/11/2017

Accepted: 10/01/2018

Published: 15/03/2018

Correspondence: Mónica Matellanes Lazo

mmatellanes@uemc.es

Alba Villota Mancebo

avmancebo@gmail.com

Raquel Fernández Merino

rfernandez3223@gmail.com

1. INTRODUCTION

Spanish consumers are modifying their shopping habits on consumer products. As explained in an article published by “The World” In 2015, Spaniards visit establishments more frequently in the second quarter of 2015 than in previous periods. In addition, the profile of the consumer has also varied, as well as the purchase channels. The Internet is one of those responsible for these changes, because it brings closer to a large number of buyers products that, without their existence, would be out of reach.

The economic situation of recent years is one of the most important variables when trying to explain the growth that distributors’ brands have undergone. As a result of the recession, families have suffered a decline in income, which has contributed to their saving as much as possible in the purchase of the products with which to fill their shopping cart. According to Frank Vingnard (2015), he assures that consumers are now more responsible and rational than in previous years.

In this sense, it is important to highlight that white brands are no longer perceived as inferior brands as compared to the brands of the manufacturers themselves. Consumers distrust more, and, therefore, they worry about being better informed and thus being able to make the best purchase decision. Advertising and different marketing strategies are some of the aspects that have caused mistrust to increase, as consumers begin to be saturated with so much claim and advertisements that appears in all types of media or channels. Current advertising is characterized by offering products that provide experiences and sensations and not so much by communicating their attributes.

White brands have been consolidated in the Spanish market, especially those that market food products. Thus, the food industry is one of the pioneers in including distributor brands in its establishments and Great Britain was the country in Europe that started working with these brands.

According to a study by the University of Alicante realized by Araceli Castelló Martínez in 2011, Spain was the second country with the largest market share of private label brands in Europe, second only to Switzerland. Obviously, a moment and a situation of total economic and financial crisis worldwide

Another aspect that must be taken into account is the creation and management of branding in these distribution products. A decade ago, this branding was very little worked and was one of the main differences compared to manufacturer brands. Currently, supermarket chains have products in their lines that are very similar to traditional brands and the designs are much more creative and original. White, simple packages and with basic packaging have been transformed into more striking packages, labels and brands in the line of large surfaces.

Do not forget that, in this type of consumer products, the recommendations by prescribers are very important and greatly determine the acquisition of some products or others. The consumer has to choose a shopping center where they can buy the products that satisfy the need to feed, a matter of basic first necessity. As a consequence, the different supermarket chains compete to attract consumers to their stores and prevent them from coming to the competition. This way, in its commercial and marketing strategy, one of the strong points to work is the direction, management and distribution of white brands.

Marketing is a discipline at the service of all brands and / or companies and it is not enough for the food sector to produce and market products, but it also has to fight to reach the minds of consumers and position itself; Once notoriety and that positioning in the mind of the consumer have been obtained, the next step is to be among the chosen options. For all this to be possible, it is convenient to segment the public to distinguish that group to which brands will orient their strategy. This will help to specify the brand philosophy wanted to be transmitted and modify the material aspects of the products, i.e their packaging.

On the other hand, not only must considerations of the product / brand be addressed, but on the other side are consumers, who seek to acquire a brand of safety, quality and emotional satisfaction, without forgetting the price issue. That is why the distributors work more that emotional part without leaving the functional logic of the product.

1.1. Evolution of manufacturer’s brands Vs distribution

Brands have different objectives and tasks, in addition to being the name with which certain products are identified, it can be said that brands perform functions of differentiation and guarantee, supporting the sale and facilitating the establishment of a coherent relationship with the consumer (Castelló Martínez, 2011).

It must be borne in mind that today consumers have a great capacity to intervene in terms of the reputation of a brand and the assessment of its use, since they have at their disposal to share or disseminate both positive and negative opinions in a quick and instantaneous way to a multitude of publics through the Internet. This is important when evaluating a commercial strategy based on white brands.

The rise of these brands has meant structural changes, changes that affect logistics, organization, production, product traceability, marketing mix, planning, distributors and consumers. An accumulation of factors that must be well coordinated and managed so that finally a white brand is successful.

Years ago, when the brands of the distributor or white brands did not represent any danger to the manufacturer’s brands, they were characterized, among other things, by (Fantoni, 2005, p. 110):

A packaging and austere, economical label, almost always blank.

Price as the only factor to compare.

Products perceived with lower quality

These are some of the features that identified the first stage of distributor’s brands. In later years, there were some changes, and the majority strategy at this time was me-too, as pointed out in the study by the University of Alicante in 2011. The me-too strategy is to copy what manufacturer’s brands do, but without making any investment in advertising or promotional actions, that is, only imitate and apply what others do with their own brand. It could be said that it is an application of the process called benchmarking very focused and used in business management.

At the beginning of the 21st century, white brands have begun to realize the need to invest in advertising and, above all, to provide their brand with an image and values ??that allow it to differentiate and position itself in a market that is often saturated. It has been a battle that has played especially with the price variable, since it is one of those that most affect consumers when making the purchase decision.

The boom of white brands in the food sector has come to boost the development of different factories that produce food without their own brand. These companies, in the 1990s have chosen to be available to different distribution chains, so that their products are created for these organizations, instead of having their own identity. It is the example of Grupo Siro that works for the number one distributor in Spain, which is Mercadona, through its white brand hacendado. The words of the Chairman of Grupo Siro are evident and clear (2016):

Hacendado is not a white brand, it is one of the most important in this country and I am very proud to manufacture for Hacendado. It is my brand. We are currently Mercadona’s suppliers in the cookie, bread, pastry, pasta, pastries and cereals businesses (Juan Manuel González Serna).

According to statements by Jaume Betrian (2009), the economic crisis posed a great threat to all companies, since people only looked for low-price products with which to satisfy their most basic needs. This expert believes that the consumer values, rather than the price criteria, promotions and distributor selection. Therefore, the strategies of manufacturers should aim to discover what the differential elements of each organization are, to know the reasons that make their products somewhat better as compared to the competition and as compared to distributor’s brands.

1.2. The success of Mercadona

Regarding the success of Mercadona, an online study by “ABC” in 2012 indicates that the price factor, the accessibility of its stores due to its successful strategic locations and its total quality management are its most valued aspects and that have significantly influenced the good valuation of consumers throughout Spain.

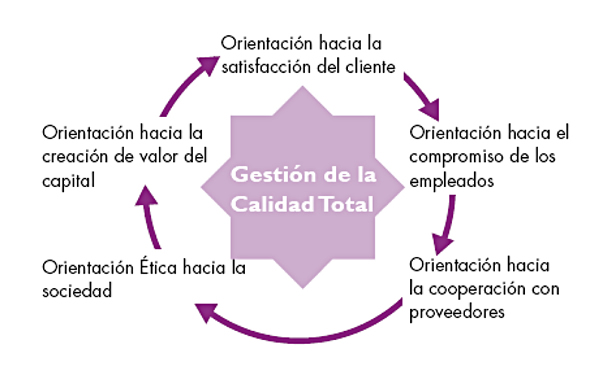

In its management model, two basic ideas can be highlighted: Total Quality and Always Low Prices. Through this approach, management gives a multidimensional content, in which it seeks excellence throughout the entire value chain of the company, always oriented towards the market and the client.

The basic points of this Total Quality Management model are the orientation to external clients and stakeholders, internal cooperation and teamwork, leadership and commitment of management, management by processes and systems, management by facts or based on information, orientation to people or the internal client, learning, innovation and continuous improvement, the development of alliances, external cooperation and the ethical approach.

Its objective is to achieve a triple purpose: create value for all stakeholders, achieve competitive advantages and differentiated subtractions on competitors and configure a culture, organization and management style that encourages commitment, participation and internal cooperation.

In summary, the Total Quality model is based on two considerations: On the one hand, recognizing that there are social responsibilities before stakeholders , consumers, supplying employees and society and, on the other hand, the importance of the leadership of senior management, and it is possible to motivate all agents to share their social vision and act in accordance with it. Next in figure 2, Mercadona’s strategy is shown schematically in terms of total quality management:

Figure 1. Total Quality Management

Source: Universia Business Review 2015

On the other hand, the strategy of always low prices (SPB) allows saving in the total sum, that is to say, in management of application of margins and savings systems in the commercial negotiations, so that there are not many price variations for the final consumer. In the beginning, the objective was to implement a model based on the stability of prices, suppliers and workers and thus to get loyal customers. The idea of always low prices is achieved by means of pressure to suppliers. Thanks to this system, customers attracted by these prices not only acquire prices on offer but they also access other higher priced products and thus obtain higher profit margins.

At present, Mercadona enjoys good stability and pricing, achieving an optimum share of loyal and fixed customers who know what they will find on the distributor’s line.

1.3. The Visual Identity of Shopping Centers

All industrialized countries look for the way to succeed, that is why, besides the commercial strategies, the techniques to carry out the Corporate Identity strategy are vital to achieve differentiation and good positioning in the market (Conesa García, 2008).

The author Costa (2006) maintains that the little importance given to the image and corporate identity is due to the fact that the concepts of identity and image are subjective concepts, and that this is an elusive, intangible matter; they are not things or products: they are impressions, meanings, information and values.

Costa (2008) and the author Lambin (2003) agree that it has been verified in European and Latin American companies that at least 10% of the company’s profits are derived from the strength of the image and they are close to 15% in the case of service companies. The performance of identity and image are shown in three essential sources; the ability to attract customers, which is not only derived from commercial activity, the ability to retain them and cultivate their loyalty, and the ability to cross-sell as a result of the image-brand relationship.

For this reason, the name, the symbol and the logo, as well as the typography and colors are essential elements that make up the corporate visual identity (González Solas, 2004: 98).

The name Mercadona is a four-syllable word, which is composed of two words: Market and Woman, with this it highlights the scope of action and the objective of the company, although today it would be labeled as implicit machismo. The study conducted by Zenithmedia highlights that the white brand Hacendado is the most mentioned in Spanish conversations

2. OBJECTIVES AND RESEARCH METHODOLOGY

This section includes the main research objectives and the explanation of the methodology applied and the justification of the sample.

2.1. Objectives

The main objective is to analyze the degree of knowledge and image of the Valladolid population about white brands in the food sector. Other objectives are:

Study the main factors that consumers take into account when choosing or rejecting a product of the distributor’s brand.

Identify which white brand is the most consumed, and why.

Study which category of white brand products are most consumed in the food sector.

2.2. Sample and chosen technique

For convenience, ease and knowledge of the market for the three researchers residing in the town of Valladolid, it was decided to select a local sample in this Castilian-Leonian city. In addition, in recent years there has been an increase in the supply of surfaces and supermarket chains in which it is increasingly common to find white brands in a consumer market that used to be conservative and distrustful.

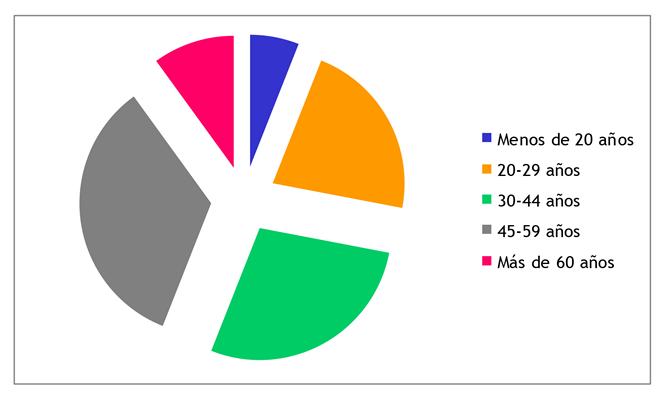

The technique of the self-administered survey has been chosen and distributed randomly in the vicinity of supermarket chains and distribution centers. The survey was carried out by 100 consumers, of which 59 were women and 41 were men. In addition, responses have been collected from all age groups, taking into account that this section was segmented into the following age groups:

Less than 20 years

From 20 to 29 years old.

From 30 to 44 years old.

From 45 to 59 years old.

More than 60 years old

The criterion of having segmented in these age groups has its justification in the segmentation used by INE in its respective surveys. The graph 1 shows the distribution of respondents regarding this variable.

The distributed survey is very brief and simple so that it is quick to answer by the consumers; this way the flight of respondents was avoided. It initially consists of three sociodemographic questions (listed below) and they have been completely anonymous. Then respondents were asked if they had any knowledge of a white brand, what white brand they consume more and why, factors that influence the purchase of white brands and finally what type of products they buy with this type of brand. The 100 surveys were distributed in the months of April and May 2016, from Monday to Friday and during the morning from 10 a.m. to 1 a.m. In this aspect, it can be considered a risky bias since in this time slot you can find a more particular and specific consumer profile (the type of a profile of a housewife woman). However, different types of audiences according to age, gender and employment status have been found as shown by the data.

The carried out survey is intended to evaluate and analyze both the situation of the white brands and the perception consumers from Valladolid have about them. To this end, this quantitative research of different ages has been carried out, trying to represent a small market niche that can humbly represent the market of consumption of white brands in a local area of Castilla and León.

The selected technique, that is to say, the survey has allowed us to know more in depth the perception of the consumers about the white brands. This way, it has been possible to understand the degree of consumption, fidelity towards these products, as well as the reasons that motivate their purchase and what their preferences are.

Graph 1. Distribution by age groups

Source: Self-made based on the survey data.

It is important to point out that the first age group has a much smaller representation, but this is also due to the fact that young people under 20 years are not usually those who make the basic purchase of food, although they are influential and decision makers in the process of said purchase. It is convenient to keep them in mind since there are times when these people live abroad, because they study in a city other than their own. As can be seen in figure 1, the most surveyed segment is the one from 45 to 59 years, followed very closely by the immediately previous one (from 30 to 44 years).

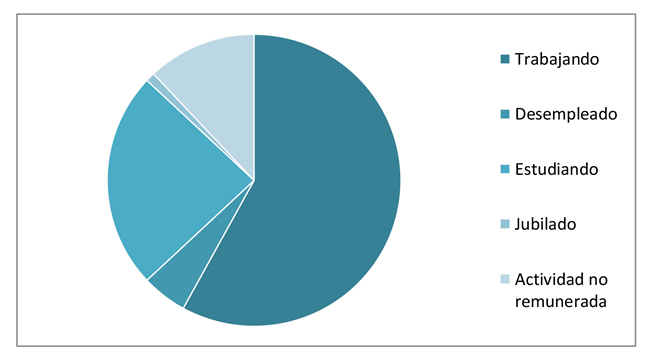

The employment situation of each person is also an important factor to take into account, since it is one of the situations that most likely affect the type of products and brands they consume. The fact that white brands have a lower price may make them more attractive to the unemployed group. But the results provided by the survey show that more than 65% of unemployed people claim to have increased their consumption of white brand products in the wake of the economic crisis.

The Graph 2 shows the distribution of the sample, in terms of their employment status.

Graph 2. Distribution by employment situation

Source: Self-made based on the survey data.

In order to arrive at more conclusive results, they will be shown by sex and age groups, since we will be able to observe the differences between these groups, not only taking into account one variable but both at the same time.

Table 1. Distribution of surveys conducted by sex and age

Source: Self-made based on the survey data.

Previously, before distributing the survey to consumers, it was applied to a representative and small selection in order to detect possible drafting and comprehension errors.

3. ANALYSIS AND RESULTS

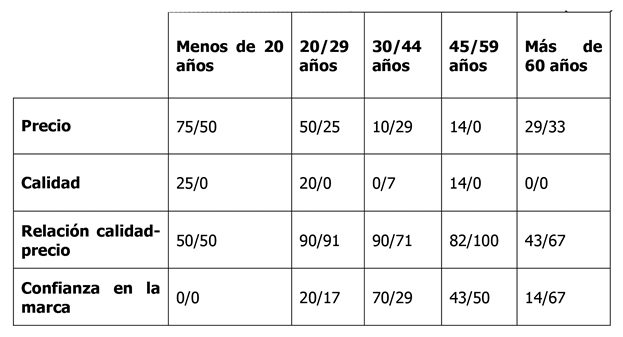

The following table 2 collects the data in percentages on the reasons why consumers consume white brands. The percentages collected in pink are the data of the female gender; while the ones in blue are of men. The choice of this table is motivated because it allows us to compare one gender and another, as well as taking into account the different age groups at the same time.

Table 2: Reasons why white brand products are consumed (in %)

Source: Self-made based on the survey data.

As you can see, the criterion of quality-price relation is one of the most outstanding valuations among all age and gender groups. Confidence in the brand being the next most voted by the most adult ages from 30 to 60 years. Evidently, the youngest (less than 20 years old) choose the price criterion as the first option that influences them when choosing a white brand.

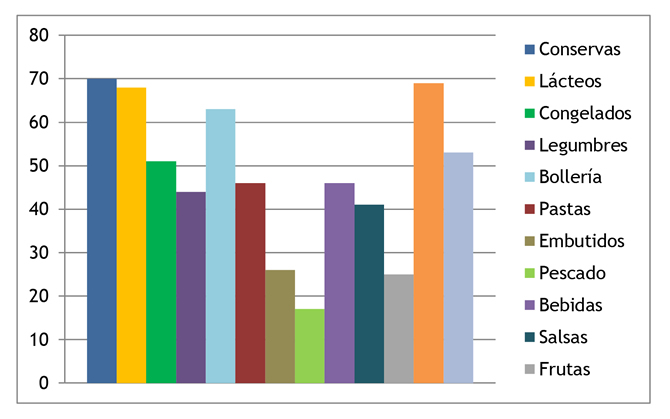

In the following graph 3, the categories of products most purchased with white brand are detailed by the sample that represents the population of Valladolid. It can be observed that preserves and snacks are the products with the highest penetration, reaching nearly 70% favorable responses. The products that, on the contrary, obtain lesser acceptance are fish and sausages, as well as fruits. Perhaps this is due to the fact that, when dealing with fresh products, they are usually purchased by tradition in specialized places close to the neighborhood of one’s lifetime. In addition, it must be taken into account that the city of Valladolid is a medium-sized town with around 375,000 inhabitants (not counting the poor quarter) that have the settled customs of buying the freshest products in the market of one’s lifetime and more specifically among the older population.

Graph 3. Categories of white brand products most consumed in Valladolid (in %)

Source: Self-made based on the survey data.

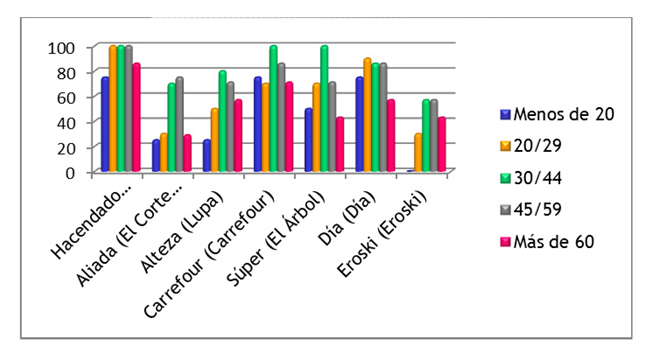

Graph 4 shows the percentage of women who say they buy or have bought products of distributor’s brands at some time. As can be seen, Mercadona stands out from the others, although if the age groups are valued, it can be concluded that there are fewer buyers among the younger population. Another brand that stands out is the Carrefour distributor’s brand; we must bear in mind that they are the two distribution groups with more presence and importance in our country. In addition, it should be noted that the El Árbol supermarkets have just been acquired by the distribution brand Día (well known and positioned among the population of Valladolid).

Graph 4. Percentage of female buyers by age group (in %)

Source: Self-made based on the survey data.

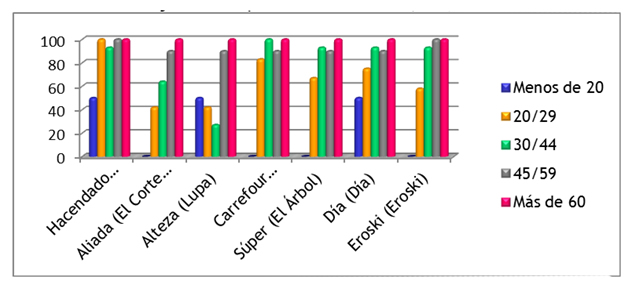

Regarding male buyers, differences are observed in the age range under 20 years; since this age group does not buy brands like Carrefour, Aliada, Super or Eorski. On the other hand, from the age of 30, you can see that they buy all kinds of white brands, Hacendado being the most bought by all age groups.

Graph 5. Percentage of male buyers by age group (in %)

Source: Self-made based on the survey data.

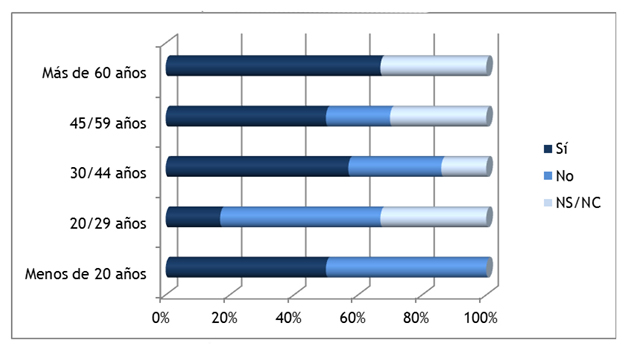

Below is graph 6 which details the influence of the economic crisis on the increase or not of consumption of white brands by the chosen sample.

Graph 6. Increase in the consumption of white brands as a result of the economic crisis by age groups (in %)

Source: Self-made based on the survey data.

In general terms, it has been possible to see that the financial economic crisis has notoriously influenced the purchase of white brands, except for the age range of 20-29 years, although it must be remembered that the data must be taken with some caution, since it is a sample that does not represent 100% of the entire population of Valladolid. However, they are clear and logical results at a simple glance that show how these brands have gained weight and sympathy among the Spanish population due to circumstances external to the food distribution sector.

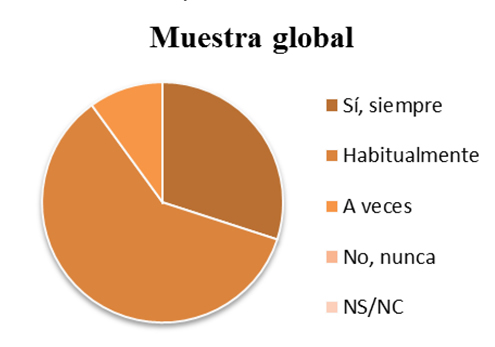

In graph 7, the frequency with which purchases of white brands are made by the whole global sample is shown, the percentages obtained are quite positive for the purchase of said white brands.

Graph 7. Frequency of purchase of white brands of the entire sample

Source: Self-made based on the survey data.

A high percentage usually buys (around 60%), while 15% does so at times, but very regularly, and 25% always does.

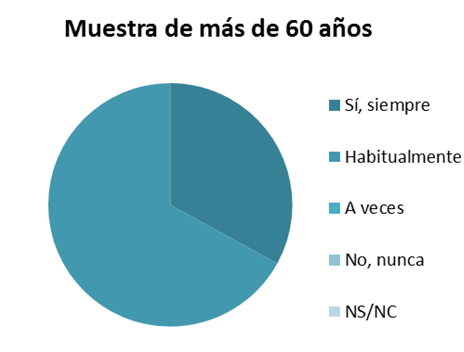

In this last graph 8, it is observed how the population over 60 years habitually buys 70% of white brands and 30% of them always do so. This age range being those that more white brands or distributor’s brands buy.

Graph 8. Frequency of purchase of white brands by consumers over 60 years of age

Source: Self-made based on the survey data.

Finally, these results indicate that, in the city of Valladolid, most of the people who know the white brands of the main supermarkets have bought them at some time; be it the brand Hacendado, Carrefour, Highness, Super, Allied ... etc, these brands being fairly well known among age groups from the age of 20. In this market of white brands, Hacendado is the one that obtains better results, getting to be the best positioned and settled among the Valladolid society.

Also obtained as results, although off the record in conversations with customers outside the survey, the packaging of products of the distributor’s brand is less careful than that of the manufacturer’s brands and the most demanded products are the preserves and appetizer, leaving out the freshest products that provide greater involvement in the purchase process since they require higher confidence on the part of said consumers.

4. CONCLUSIONS

In general, it has been known that most respondents know white brands and consume them; all this being influenced by the financial economic crisis that unfolded in Europe in 2008. If you relate the price factor that is the most valued variable of white brand products, it can be said that the fact that they have a lower price has made they become much more attractive products to all consumers who have seen their available income reduced due to this economic crisis.

This consumption of white brands is understood as a market that has already little to envy to the manufacturer’s brands, since they compete in equal conditions on quality and design of package and packaging.

On the other hand, the white brand Hacendado of the Mercadona distributor is the best known among all consumers and the most bought, both by men and women. It has a very good notoriety and recognition. Carrefour, for its part, is close to it as the second sales distribution center, as well as at the level of knowledge.

The frequency with which surveyed consumers claim to buy these products is quite high. Almost all of them opt for the answers “sometimes” or “usually”, so it can be concluded that they acquire them either every week or at least once a month and with certain regularity.

The criteria that motivate these purchases could be grouped into two large blocks, on the one hand, quality and, on the other hand, price. As commented by most of those who have composed the sample, the relationship between both variables makes these products very attractive.

As it has been previously specified, the quality these white brands are getting is quite good, obtaining a great acceptance among consumers and also taking into account that the price is lower than that of the manufacturer’s brands. On the other hand, it can be said that packaging, although having experienced some improvement in the last generations of these white brands, is still considered a weak point, on which they should probably continue working. Do not forget that distribution companies invest very little money in the design of their products, although this trend is declining in recent years. Formerly, containers used to be white or black without too many illustrations and with a very basic typeface. The container and packaging currently remains one of the variables worst rated by the population but, in reality, the profile of the white brand consumer is not guided by aspects such as design; instead, the consumer seeks a good harmony between quality and price in brief.

It can be said that the most consumed products within the white brands of the food sector are the preserves, appetizers, dairy and pastries, being far above other categories such as fish, sausage, vegetables or fruits. All this is evident, since these are products that require more specialized and serious involvement by the consumer in the act of purchase, in addition to being fresher products.

Anyway, one of the important considerations of this article is that customers from Valladolid who have ever bought white brand products claim to be willing to repeat the purchase. It is a very remarkable factor since every brand seeks to repeat purchase and to retain consumer loyalty for life. If the brands do not achieve this, they will fail and would need other actions to be able to survive. Therefore, any white brand strategy goes through achieving this desired loyalty that the entrepreneur wants. And it is that the perception of a white brand, as a distinctive feature of quality in relation to price, makes its attributes position in the mind of consumers in such a way that they assure to be willing to repeat the purchase of the same products.

It should also be noted that most white brand consumers consider that, although two products are made by the same company, considering one as a white brand and another as a manufacturer’s brand, they are not exactly the same. It is evidence that the consumer knows, in a generalized way, when he is asked or gives testimony of his degree of knowledge. In fact, it does not mean that the products of white brands do not have quality and are not good, but that the raw material may come from another place as it happens with the production and distribution of milk. Sometimes, the same milk plant distributes for white brands and for manufacturer’s brands; the difference is in the type of cow since some come from the zone of origin of Asturias and others from Zamora of the region of Castilla y León, but this does not mean that they do not pass the minimum control of quality levels, although It is well known that Asturias cows graze differently than Zamora cows and this affects the type of raw material they finally offer.

5. REFERENCES

1. Aaker, D. (1996). Construir marcas poderosas. Barcelona: Gestión 2000.

2. Artículo de ABC (2012). Las claves de éxito de Mercadona. Recuperado de http://www.abc.es/20120314/local-comunidad-valenciana/abci-mercadona-201203141102.html

3. Artículo de El Mundo (2015). Internet, marcas blancas y segunda mano, la diana de los consumidores. Recuperado de http://www.elmundo.es/economia/2015/10/14/56151c99268e3e4d2f8b4667.htm

4. Blanco, M. y Gutiérrez S. (2015). Modelo de Gestión de Calidad Total en el Sector de la Distribución Comercial en España: El Caso Mercadona. Universia Busines Review. Primer Trimestre 2015.

5. Castelló Martínez, A. (2011). La batalla entre la marca de distribuidor (MDD) y marca de fabricante (MDF) en el terreno publicitario. Recuperado de http://rua.ua.es/dspace/bitstream/10045/26809/1/Pensar%20la%20publicidad_Araceli%20Castell%C3%B3.pdf

6. Cervera Fantoni. A.L. (2005). Envase e Imagen de Producto. Madrid: Esic.

7. Conesa García, Mª Pilar (2008). Administración y Dirección de las Organizaciones: Una visión Humana. Valencia: Universidad Politécnica de Valencia.

8. Costa, J. (2006). La Imagen Corporativa en el Siglo XXI. Argentina: La Crujía ediciones.

9. Estudio del Informe Kantar World Panel (2015). Recuperado de http://www.kantarworldpanel.com/es/Noticias/Las-marcas-de-Gran-Consumo-mas-compradas-en-Espana-

10. González Solas, J. (2004). Identidad Visual Corporativa, La Imagen de nuestro tiempo. Madrid: Síntesis.

11. González Serna, J. M. (2016). Página web de Grupo Siro: http://www.gruposiro.com/

12. Lambin, J. J. (2003). Marketing Estratégico. Madrid: Esic.

13. Martínez Olmo, F. (2002). El Cuestionario. Madrid: Laertes.

14. Memoria anual Mercadona (2013). Recuperado en: https://www.mercadona.es/corp/esp-html/memoria2013.html

15. Página web de Mercadona: www.mercadona.es